Why These Three Numbers Matter

A meaningful shift is underway. Women tend to live longer than men—by about five years on average—which means their money may need to last longer. At the same time, women are expected to control a growing share of wealth, with projections suggesting they may manage roughly 45 percent in the years ahead. And by age 59—the average age of widowhood—many women find themselves making financial decisions on their own.

Each of these trends carries practical implications. Together, they can be viewed through three numbers shaping many women’s financial lives:

- 5

- 45

- 59

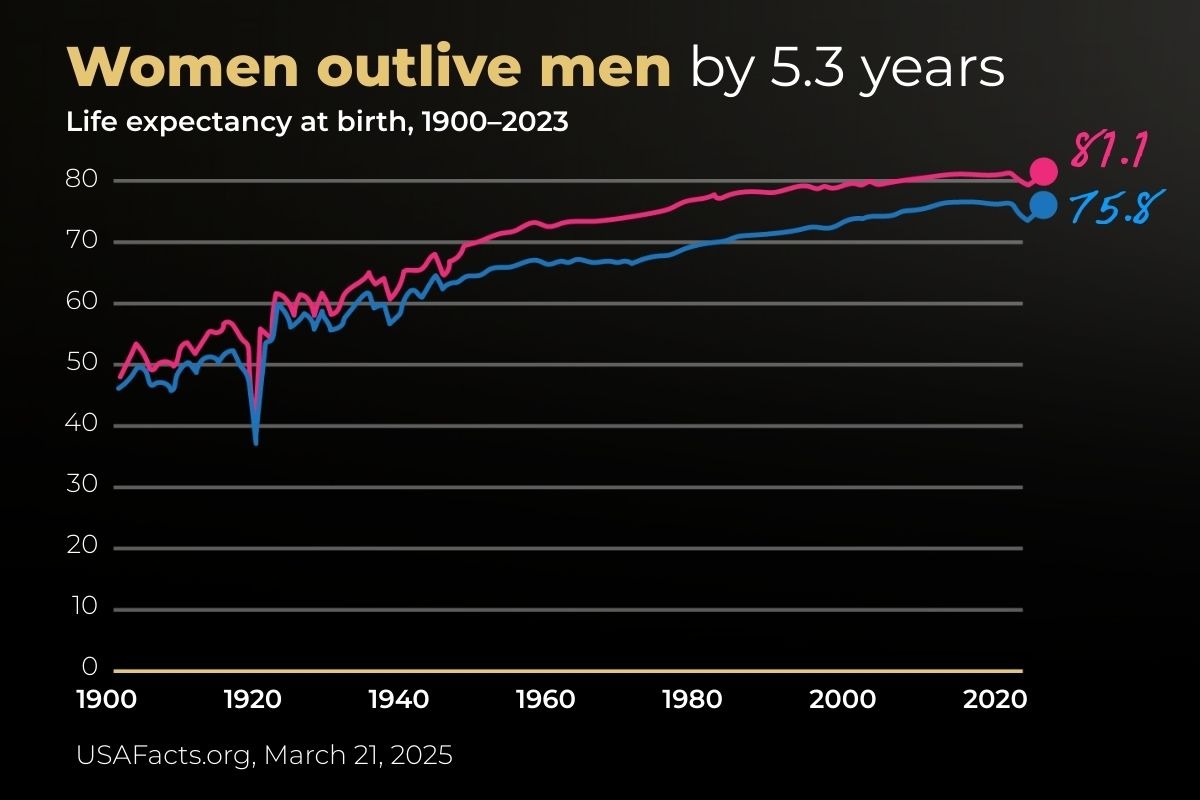

5 - The Number of Extra Years Your Money May Need to Last

On average, women in the United States live about five years longer than men. While both men and women are living longer than at the beginning of the last century, a gap remains. In the U.S. in 2023, the life expectancy for men was 75.8 years. For women, it was 81.1 years.1

Other studies show that many of those additional years are spent managing health concerns. On average, women not only live longer, but also spend more years with chronic conditions, increasing the need for ongoing healthcare and caregiving support.²

While longer life expectancy is good news, it carries clear financial implications:

Retirement may last 30 years or more.

Healthcare costs often rise in your 70s, 80s, and 90s.

Periods of reduced work or caregiving—sometimes well before traditional retirement—can affect earnings and long-term savings.

Planning for the Extra Years

Living longer can affect how you plan for income, savings, and healthcare. Because women often live several years longer than men, it can help to plan with those extra years in mind. A few considerations include:

Plan on paper to live until at least age 95, even if you don’t expect to live that long. It is usually easier to adjust if you have more than enough later in life than if you come up short.

Think about your money in stages—for example, funds for the next five to ten years, funds for later years, and a separate amount set aside for healthcare or extended care.

Review your plan from time to time and ask how it would hold up if you live longer than expected, if healthcare costs rise, or if investment returns are lower than average.

45 - The Share of Investable Assets Women Are on Track to Control by 2030

One study suggested that women may control as much as 45 percent of all investable assets in the U.S. and Europe by 2030.3

At the same time, income patterns within families have shifted:

In 16 percent of opposite-sex marriages, wives are the sole or primary breadwinners—about three times the share from 50 years ago.⁵

In 29 percent of marriages, both spouses earn about the same income.⁵

Just 55 percent of marriages today have a husband as the primary or sole breadwinner, down from 85 percent in 1972.⁵

In 2023, 45 percent of mothers were breadwinners—either single mothers or married mothers earning at least half of their family’s income—and another 24 percent were co-breadwinners.⁶

Taken together, these trends reflect a clear shift: women are receiving a growing share of wealth, and their earnings play an increasingly central role in household finances.

What Does This Mean for Financial Strategy?

For women who manage investments—or expect to inherit them—these trends raise practical questions. Is there a clear investment plan that reflects personal goals, time horizon, and comfort with risk, or has the portfolio grown over time without a unified strategy? If a woman is the primary or co-earner, is the financial plan built around her income, her partner’s income, or both? And do estate documents and beneficiary designations make it easier for a surviving spouse to manage and transfer assets?

With those questions in mind, a few practical steps to consider include:

- Creating or updating a personal investment policy statement that clearly defines goals, time horizon, risk limits, and the decision-making process—particularly if family wealth may eventually be managed independently.

- Consolidating or coordinating scattered accounts so retirement assets, inherited funds, and taxable investments align under one consistent approach.

- Reviewing and adjusting insurance coverage and emergency reserves, especially for primary earners, to ensure they reflect household income and those who depend on it.

These are not dramatic changes, but thoughtful adjustments that can help build clarity and confidence over time

59 - The Age Many Women Face Widowhood

Mortality is a difficult but necessary topic for everyone. However, married women, in particular, may benefit from being financially prepared for the possibility that they will outlive their husbands.

Sobering Facts Around Widowhood

- The average age of widowhood for women in the United States is 59.7,8

- About 34 percent of women aged 65 and older in the U.S. are widows, rising to 58 percent for women aged 75 and older.

- Nearly 700,000 women lose their husbands each year in the U.S.

- Women live 12-13 years on average as widows.

- Household income for women can fall anywhere from 37 percent to 50 percent after the death of their spouse.

- Upwards of 40 percent of widows report not being confident in their ability to manage finances alone.

- Within 12 months of becoming a widow, 45 percent of women experience a decline in their standard of living.

- Half of all widows lose 50 percent of their household income upon the death of their husband.

- Widows who employ a financial professional before their loss are 90 percent more likely to feel more prepared.

Women between ages 55 and 64 spend an average of about 10 years as widows.⁸ As a result, many may find themselves fully responsible for their finances sooner than expected—often while still working or helping support adult children.8

What This Means for a Financial Strategy

For many married women, these numbers point to the likelihood of becoming the sole decision-maker for family finances at some stage of life—even if a partner manages most of it today. That raises a practical question: is it better to sort through and organize everything during a time of loss, or to be prepared in advance?

Preparation can be framed around three simple ideas: clarity, control, and continuity.

Clarity: Keep a current list of accounts, insurance policies, legal documents, passwords, and key contacts. Make sure the information is up to date, and that both partners know where to find it. Review it together from time to time.

Control: Consider whether account ownership and access reflect your role in the household. Where appropriate, being a co-owner rather than only a beneficiary may simplify matters later. Both spouses should understand how retirement income is generated, how bills are paid, and how taxes may change if one spouse passes away.

Continuity: Build relationships with trusted professionals—such as a financial advisor, estate attorney, and CPA—so you are not starting from scratch if you become the sole decision-maker. Asking questions now, while both partners are present, can make future transitions smoother.

The numbers 5, 45, and 59 are not abstract statistics. They reflect real shifts in longevity, wealth, and responsibility. Together, they suggest that women are likely to oversee more assets, for longer periods of time, and often independently.

Keeping these realities in mind can help guide thoughtful planning—so that financial strategies align not only with today’s circumstances, but with the years ahead.

1 USA Facts, March 21, 2025

2 The Guardian, December 11, 2024

3 McKinsey & Company, May 8, 2025

4 Diversified Trust, October 13, 2025

5 Pew Research Center, April 13, 2023

6 Center for American Progress, May 9, 2025

7 Gitnux, December 11, 2025

8 Resto NYC, October 12, 2023