Much of the retirement planning process focuses on ensuring the numbers work. Over time, people work toward “their number” — the amount needed to retire comfortably and confidently. By the time retirement approaches, savings are often in place, investment accounts are organized, and an income strategy is established. On paper, everything looks ready.

What tends to receive far less attention are the conversations about what retirement will actually look like once the working years end. Not the math, but the life itself. How do you want to spend your time? What are you looking forward to? What does a good week look like? And are the two of you imagining the same version of retirement?

Those conversations are harder to define than the financial side of retirement, but they often matter just as much. Many couples spend years preparing financially for retirement without ever really talking through what they want this next chapter of life to become.

Fidelity’s 2024 Couples and Money Study, which surveyed partners separately, found that many couples are not fully aligned on key financial and retirement questions. That disconnect often extends beyond money itself. Even when the planning is solid and the numbers work, couples may still have very different expectations for what retirement is supposed to look like once they get there.1

The Timing Problem Not Talked About Until It’s Too Late

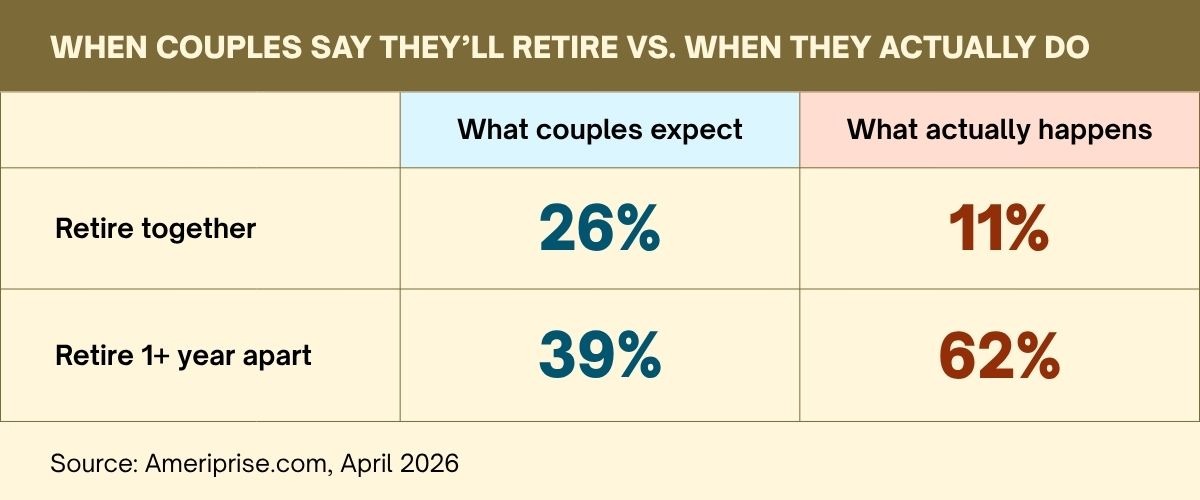

More than two-thirds of working couples expect to retire at the same time or within a year of each other, according to Ameriprise Financial’s 2024 Couples, Money, and Retirement study.2

It’s a common assumption couples make and one that rarely comes true.

The gap between expectation and reality here is not just a scheduling inconvenience. When one partner retires, and the other does not, the household dynamic changes in ways many couples are unprepared for. The retired partner may lose some professional identity and daily structure. The still-working partner may come home to a different kind of pressure. Who manages the house? Who handles the money? What does the retired partner do with eleven hours of unstructured time?

None of these questions is unanswerable. But they can be much easier to answer before one person has already retired than after. A staggered retirement, intentionally planned and with a clear purpose, can be a smart financial strategy. The working partner can continue building savings, delay Social Security benefits, and maintain health coverage. But when it happens without much discussion beforehand, the same situation can create friction that is difficult to unwind.

One of the more valuable conversations couples can have in the years leading up to retirement is this: What happens if we do not retire at the same time, and what does each of us need and expect if that is the case?

Questions Worth Asking Before You Retire

Several important questions can reveal differences in retirement expectations that many couples have simply never had a reason to talk through before. Here are five worth discussing together as retirement gets closer.

Where Will We Live, and Have We Both Truly Agreed?

This may be the retirement conversation with the biggest financial impact — and often the one couples spend the least time talking through. One partner may picture a warmer climate. The other may assume they are staying in the family home. Cost of living, proximity to children and grandchildren, healthcare access, and what happens to the house all depend on this question having a real answer, not an assumed one.

How Will We Build Meaningful Structure in Retirement?

Retirement removes the structure that most people have used to organize their lives. For some people, that's a relief. For others, it's destabilizing in ways they did not anticipate. The couples who tend to navigate this change most smoothly are those who have already thought about what will replace work, not just financially but personally. Board service, consulting, a creative practice, a physical commitment, or a volunteer role. These are not hobbies. They're sources of identity—and worth thinking through together, especially in your early retirement years.

This may also matter for your relationship. Couples who suddenly spend every hour together after decades of parallel busy lives sometimes discover they need more intentional structure around both togetherness and individual space than they expected.

Retirement means a lot more time together—and while that's wonderful, it can also be an adjustment. Talking openly about how you'd each like to spend your days can go a long way.

How Will We Handle Healthcare, and Do We Understand What It Will Actually Cost?

A 65-year-old retiring in 2025 can expect to spend approximately $172,500 on healthcare over the course of their retirement, according to Fidelity’s 2025 Retiree Health Care Cost Estimate. For a couple, that figure climbs to roughly $345,000.3 These estimates assume enrollment in Medicare and do not include long-term care.

What surprises most couples is not the healthcare number itself but the complexity of getting there. Medicare decisions are not simple. The income-related monthly adjustment amount (IRMAA) surcharges increase Medicare Part B and Part D premiums for certain high-income enrollees. In 2026, the surcharge applies to people with a modified adjusted gross income above $109,000 (individual return) or $218,000 (joint return).4

Couples with an age gap may face a Medicare coverage gap if one partner retires before 65. And every choice involves trade-offs among premium cost, provider access, and out-of-pocket exposure, which differ across partners. A Medicare professional might offer some guidance.

What If One of Us Needs Significant Extended Care?

According to the U.S. Department of Health and Human Services, 56 percent of adults turning 65 between 2021 and 2025 are expected to need some form of long-term services and support during their lifetime.5

A couple facing extended care expenses sees their wealth decrease by an average of 21 percent over nine years, according to Morningstar research. The decisions available at 70 can be more expensive and more limited than those available at 58 or 62.6

Most couples put this conversation off, not because they do not care about the answer, but because confronting the possibility of illness can be uncomfortable. That discomfort is worth pushing through early.

The question to answer together is not "Which facility would we prefer?" It is, "What is our financial strategy if this happens, and have we done anything to prepare?"

How Will We Coordinate Social Security, and Have We Considered Both Partners’ Situations?

A Social Security claiming strategy is one of the highest-value decisions a couple makes. The timing of one partner’s claim affects the survivor benefit available to the other. Delaying benefits may increase the surviving partner's lifetime income. On the other hand, claiming early to fund current expenses may lower the investment drawdown math for the years before both partners are collecting.

While you can start claiming Social Security benefits as early as 62, doing so reduces your monthly benefit. Delaying until age 70 increases your benefit to your maximum level.

Here are the maximum monthly benefits at various ages for someone who earned at or above the taxable maximum during their career:

It’s not about finding the “best age” to claim, but rather identifying the age that best fits a couple’s personal situations and goals. There is no universally right answer. But the answer should come from a review of both partners’ earnings records, health trajectories, and income needs, not from an assumption.

When talking with your partner about claiming Social Security, consider treating it like a strategic project, not just an election on a government form. While Social Security may not be your primary source of retirement income, it can still play a significant role in a comprehensive retirement strategy.

What It Looks Like When Couples Talk About Retirement

Most couples discover that the gap between what each person wants from retirement is not as wide as it first seems. The partner talking about the beach house has often also been thinking about the grandchildren. The partner who wants to stay put may quietly be questioning how many more winters they really want to manage. The differences are real, but they usually feel less fixed once they are actually talked through.

The couples who seem to navigate retirement best are usually not the ones who agree on every detail from the beginning. More often, they are the ones willing to stay open to hearing something they did not expect from the other person. A different priority. A different concern. A different picture of what this next chapter is supposed to look like. That willingness to listen — without immediately trying to solve or defend — tends to make those conversations more productive and a little less intimidating.

Cetera Wealth Services, LLC exclusively provides investment products and services through its representatives. Although Cetera does not provide tax or legal advice, or supervise tax, accounting or legal services, Cetera representatives may offer these services through their independent outside business. This information is not intended as tax or legal advice.

1 BusinessWire.com, April 2026

2 Ameriprise.com, April 2026

3 NewsRoom.Fidelity.com, July 30, 2025

4 NerdWallet.com, January 15, 2026

5 AARP.org, March 12, 2026

6 CFSWV.com, January 2, 2024